In order to determine how much condo insurance you need in Dorchester MA, you should plan to look at your condo’s association master policy.

How Much Dwelling Coverage Do You Need?

There are two types of master policies that affect how much dwelling coverage you need. All-inclusive means that the policy insures the exterior and interior surfaces of the unit and you would just need to worry about the stuff you own. Fixtures attached to the wall, such as the shower, cupboards, and toilets, also fall under this master policy. However, improvements are considered a gray area. A bare wall in policy means that everything inside the condo’s four walls needs insurance. This means fixtures and appliances have to be covered by your individual policy. If your condo association has bare walls in the policy then you will need more dwelling coverage.

Once you have figured out what type of dwelling coverage you need you to evaluate your options with an agent at Vargas & Vargas Insurance and discuss what it would cost to recreate your condo in the event a major accident happens. You can use an estimate from your mortgage lender or an estimate from a contractor or architect. Sometimes a mortgage lender will have a requirement for the specific amount of dwelling coverage you should have. It’s important to keep your dwelling coverage updated as you make improvements to your condos, such as a bathroom or kitchen renovation since it would be a higher cost to replace these new items.

How Much Property Coverage Do You Need?

The easiest way to determine how coverage you need for your personal property in Dorchester, MA is by doing an inventory. Be sure that all your valuable items, such as jewelry, are covered.

Contact Vargas & Vargas Insurance to get a quote on condo insurance.

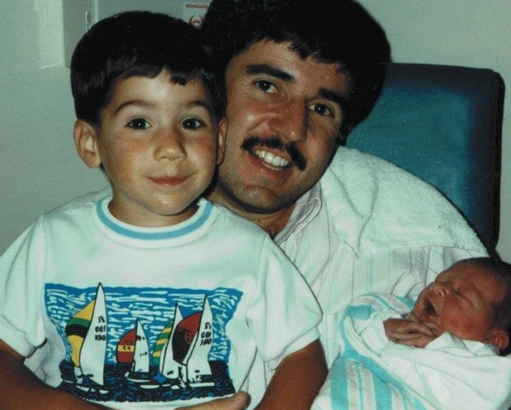

Photo taken in 1992 when Jonathan and I met his brother, Matthew for the first time.

Happy Father’s Day. I say that with no exclamation, no sense of a hearty salutation. Not that I want Fathers today to feel unloved or un-appreciated. No, not at all.

On the contrary, my lack of happy exclamation is meant to express the sobering reality of a Father’s Day in the year 2020. We live in revolutionary times, like none our Nation has experienced since its founding or since the Civil War that divided our us!

Families celebrating Father’s Day, 2020, face an entirely new set of challenges that can easily dampen their bright moods in honor or their Dads.

The COVID-19 pandemic created an entirely new dynamic for Fathers all across our great country. Dads who literally became “stay-at-home” parents, living a different existence with their children than they may have lived previously, taking on more responsibilities for the nurturing, care, and even education of their children.

Hopefully, also, coming to realize the hard work that Mothers, Teachers, Coaches, and others perform to help these Dads’ children grow into adults.

The pandemic created a new reality for families of Dads who are Essential Workers. Instances where Fathers cannot come home for weeks or months due to their responsibilities to their respective communities out in the world, and, for the protection of their children and wives.

The political climate can be a daunting experience on this Father’s Day too. Families may find themselves divided along stark lines of opinions and affiliations, bringing long-simmering tensions to the surface.

Finally, the Black Lives Matter dynamic presents Fathers everywhere, of every race, creed, ethnicity with distinct daily challenges to face compassion for fellow humans.

While this message may seem sobering to you, I believe the true takeaway is one of hope. Father’s Day is an institution in The United States, one created as a response to Mother’s Day in the early Twentieth Century, to create an equal opportunity to honor Fathers in the same way we honor Mothers.

And there, that is the sense of hope I find for this Father’s Day, 2020. The American Family is an institution, no matter how that family is constructed, and the American Family is something to honor, to hold true to our hearts, and to believe in as we search for something of certainty during these challenging times. On this Father’s Day you can find strength, hope, and, yes, a sense of optimism, that our great American experience will respond to these challenges and we will all be the better for it, all of us, Families, Mothers, and, yes, Fathers.

Unexpectedly finding yourself paying for forced place insurance can create a significant dent in your monthly budget. This type of insurance is a lender’s response to expired or insufficient insurance, and it costs significantly more than your own policy. It sometimes as much as four times the cost of your own policy. Fortunately, there are steps homeowners can take to resolve their current insurance deficiencies and request that their lenders remove the forced place insurance policy.

What Is Forced Place Insurance?

Forced place insurance is an insurance policy that your mortgage company purchases to cover their interest in your home if:

You let your home insurance policy expire, or

Your policy does not meet their coverage requirements.

Forced place insurance generally only covers the cost of your mortgage. While other insurance policies cover your possessions and the full cost of replacing your home, as well as protect you in the event of a lawsuit, forced place insurance does not protect the homeowner and only replaces the cost that protects your bank or mortgage company.

Why Is Forced Place Insurance So Expensive?

Forced place insurance is generally more expensive than regular homeowners insurance. That’s because it is an extra step that your lender needs to take if they determine that you have not met the insurance requirements specified in your mortgage. Because your property must be insured in order to protect your lender, allowing your homeowners insurance to expire — or purchasing a policy that does not meet the needs of your area — gives your lender the right to purchase any policy they choose for your property.

In many circumstances, the cost of forced place insurance can cost multiple times the amount of a typical homeowners insurance policy. Because the cost of this policy becomes the homeowner’s responsibility, most lenders will not shop around for an affordable option.

If you want to know more about forced place insurance and how to get a more favorable policy, we can help. Contact Vargas & Vargas Insurance today.

Homeowners insurance in Massachusetts is complicated. That’s why the staff at Vargas & Vargas is creating blogs. We want to help our customers understand the most important insurance topics as they relate to YOU. With this article, we’ll explain personal property insurance, also known as contents coverage.

As always, feel free to reach out to us directly to speak to a licensed agent if you have questions beyond the scope of this article.

What Is Personal Property Insurance?

Personal property coverage, or contents coverage, is a protection built into your homeowner’s policy for the contents of your home. It covers your belongings, like:

Furniture

Clothing

Carpeting

Dishes and cookware

Almost everything else you own (with a few exceptions)

Take a look around your home. What would it cost to replace everything if the home was to burn down? It would probably cost quite a bit. So most homeowner’s policies will start their basic guess of your personal property’s value at 50% of your home’s reconstruction value. In other words, if we believe your home would cost $300,000 to rebuild, we can guess that your belongings are worth about $150,000.

To get more refined valuations, keep receipts for the more expensive purchases in your home. They can be very helpful after a loss. Also, every homeowner’s insurance policy is unique. Some programs provide more contents coverage than others. So talk to a licensed agent if you feel your contents coverage isn’t enough. We can always provide more!

What Isn’t Covered?

Certain items aren’t protected by personal property coverage. The list includes things like:

Luxury jewelry

Fine art

Expensive furs

Heirloom antiques and collectibles of high value

If you own valuables like a $70,000 painting or a $20,000 Gibson guitar signed by John Lennon, then talk to your agent to get it endorsed on your homeowners policy.

But if you own a $13,000 diamond ring, you’ll need special insurance for it. This type of coverage is called a Personal Article Floater (PAF) — or simply a “floater” — in the industry. Just provide us with certified appraisals, and we’ll do the rest!

Need to talk about personal property insurance? Vargas & Vargas Insurance has service centers all around Massachusetts, and we’re happy to help. Email us today or call 617-298-0655 to speak with a licensed agent.

If there’s anything these uncertain times have taught us, it’s when massive changes come our way, we can adapt.

Confronting the global COVID-19 health crisis has brought many changes to our daily routines– including how we do our jobs. For many of us, there’s no more leaving home to go to work. If you’re now managing your business from home, these three tips can help you balance your personal and professional life.

1. Keep your routine

When work and home life blend, it can be a challenge to keep track of time and easy to get distracted. Create a pattern to your day.

For example, when you wake up:

Take a shower as you usually would

Make time for breakfast or coffee.

Exercise, meditate, or spend some time in your bliss station.

Pick an activity that helps you start your day the way you want to – even if it’s just for a few minutes

If you’re not working a set schedule remotely, try creating your own scheduled work-from-home hours. Taking time each day to “show up” for work can give you a greater sense of control in unsettled times.

2. Be creative

For some, this might be a time to explore new ways to grow your business, grow your skill sets, or launch a new idea. If you’re in that creative headspace

List ideas on paper to research online.

Reach out to experts or people in your network by phone or email.

Keep up with your customer and prospect base on social media or via email

Write a blog, email or other communication telling your customers how you’re handling the crisis

Brainstorm ideas with other professionals on ways to keep your business essential in this new normal.

Start or join a virtual coffee of cocktail hour to see how and what others are doing work from home.

3. Relax and recharge

Find ways to relax that separate work from the quality time at home.

Play games with your kids, make a meal with a housemate, or just take time out to read quietly on the couch. You can also stream exercise routines online, right in your living room, and build strength with weights if you have them on hand – or even soup cans.

Finding time to relax or exercise across each work-from-home day can be essential to creating distance from your professional tasks and having the energy to get your work done.

More than anything, find the pace and structure to the day that works best for you and your business to work from home like a pro. Set a time that your workday ends, if you don’t your work with take over your life.

4. Check-in with your clients

Make sure that your clients know you are thinking of them right now and you’re available to answer any of their questions about your business as it relates to the coronavirus. A lot of your clients might be experiencing anxiety about what comes next, and as a trusted expert in your field, you are well-positioned to guide them through challenges and changes.

Take the time to call or text each of your clients to continue building long-term trust. Send a message to cvargas@vargasinsurance.com and I will share with you the message that has been working very well for us!

As always, Vargas & Vargas Insurance your local independent insurance agency is always ready and willing to help, you can reach our team at 617-298-0655.

It’s tax time! At Vargas & Vargas, we’re Massachusetts licensed insurance agents and tax professionals, and we’re ready to help. We want our customers to be aware of the Massachusetts “Circuit Breaker” tax credit for folks who are age 65 and up. We know that every cent counts at income tax time. This income tax credit can be valuable for seniors, whether they own a home or rent.

Seniors Might Get a Cash Refund From Massachusetts — Even If You Don’t Pay State Taxes

According to this Massachusetts Association of Councils on the Aging (MCOA) fact sheet, the “‘Circuit Breaker” tax credit program is a program for individuals aged 65 and older, whose property taxes and half of the water and sewer bills are more than 10% of their annual gross income. Renters can qualify for the credit, too, if your rent is more than 25% of your income and you meet a few other criteria.

Seniors can get this refundable income tax credit even if they owe no income taxes!

A Few Basic Criteria

This tax credit is based on property taxes you’ve paid (or that your landlord paid) in 2019, plus your sewer and water bills. Keep these requirements in mind:

You must be 65 or older this year to qualify.

Your primary residence, whether you own or rent, must be here in Massachusetts.

Your earnings must be less than $60,000 for a single individual, $75,000 for a head of household, or $90,000 for married couples who file jointly.

For instance, let’s assume you’re single and earned $40,000 in 2019. You paid $3,000 in property taxes and $4,000 in water and sewer bills. Since your total eligible payments of $5,000 are greater than 10% of your earnings, you’ll qualify for the tax credit!

How Much Is the “Circuit Breaker” Tax Credit Worth?

According to the official Massachusetts state website, the maximum credit value is $1,130. Talk to a tax advisor about the exact credit amount for your unique situation.

Vargas & Vargas is a local, family-owned insurance agency. We provide competitive insurance products and tax services across Massachusetts. Reach out to us today if you’d like to learn more about our tax services or if you need a quote for homeowners or renters insurance.

Auto insurance is not just one type of insurance. In most cases, you will need to have liability insurance coverage to protect other drivers from you and any mishap you may have. This is mandated by each state and differs from place to place. When you have a car loan, the lender will make you carry certain other types of insurance to protect them. But after your loan is paid, you can decide what other parts of auto insurance you want to carry. At Vargas & Vargas Insurance in Dorchester, MA we pride ourselves on our ability to help you solve your insurance problems at the most competitive rates available.

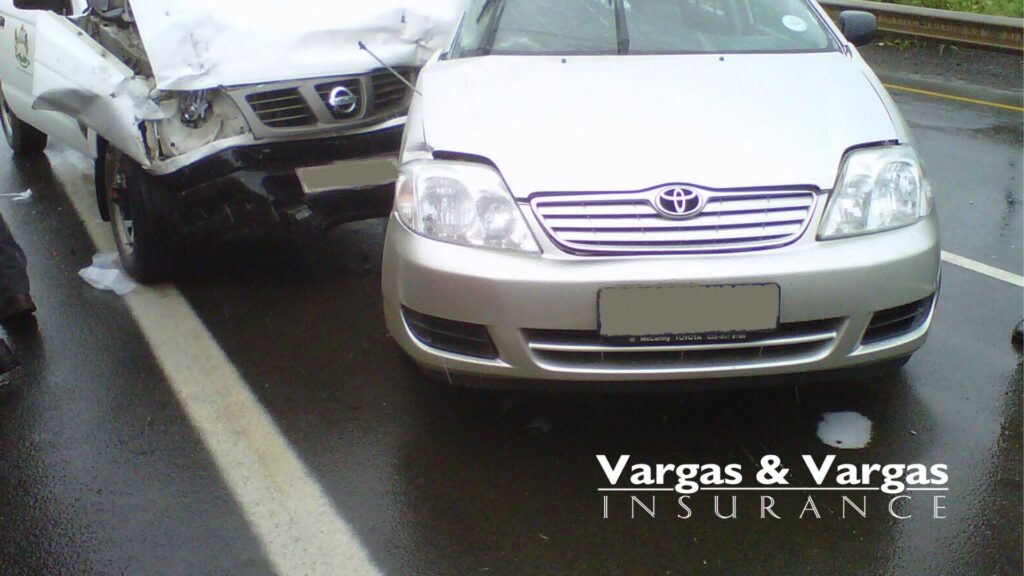

When it comes to the question do I need comprehensive coverage if I have collision coverage it is important to understand the type of coverage both of these types of insurance providers. In some ways, it is like comparing apples and oranges, the things that are covered by both types are really quite different.

Collision insurance pays for repair or replacement of your vehicle in an accident where you are deemed to be the responsible party or at least partially responsible. This is coverage that usually involves another vehicle but it can also be an inanimate object like a pole or a tree. Comprehensive is often referred to as non-collision coverage. It covers things that are beyond the driver’s control like a large animal running into the road in front of your vehicle. Glass coverage is usually also included. Comprehensive insurance includes weather events that impact your vehicle. If your vehicle is stolen or vandalized comprehensive insurance coverage will kick in.

As you see, these are both very important types of coverage and there is no overlap in the coverage. For more information about both of these types of auto insurance give the office of Vargas & Vargas Insurance in Dorchester, MA a call.

The biggest benefit of working with a local independent insurance agent like Vargas & Vargas is that our licensed local agents work with many insurance companies. We will customize your insurance policy to your own specific needs, then we can move forward getting quotes from the best companies for your unique situation.

Need some Massachusetts insurance quotes? Let’s talk!

All insurers are not created equal, nor are all insurance policies. We’re not here to sling mud or speak badly about any insurance provider! But we are going to explain how every insurance company has an ideal customer in mind, and show you some specific differences between Progressive and Geico insurance policies as examples. Our duty at Vargas & Vargas Insurance is to connect every customer with the right insurance policy. We work with many major insurance companies, and we can help take the guesswork out of any of your Massachusetts insurance policies. As always, if you have questions beyond the scope of this article, reach out to us today.

About Progressive

Progressive is a well-respected insurer with an excellent reputation. Their ideal client is a multi-line household — in case you hadn’t noticed “Flo’s” focus on insurance “bundling” in their advertising campaigns. Progressive will insure your home and autos, and the company offers life insurance choices, too. They provide great coverages for adults with multiple insurance needs.

Progressive provides homeowners insurance in-house; they don’t farm it out.

About Geico

Geico began as an insurance provider for government employees and gradually broadened their scope. Geico’s focus is providing economical pricing on auto insurance, though they also insure recreational vehicles like motorcycles and RVs. They usually have somewhat better rates for some riskier drivers, like those who have had many at-fault accidents, those with many speeding tickets, and young inexperienced drivers.

Geico does not write their homeowners insurance policies. They can provide you a quote, but they “farm out” the policy to a partner.

Our Perspective

At Vargas & Vargas, we work hard to match the right type of insurance policy to our customers. Both Progressive and Geico homeowners policies, for instance, will provide replacement cost coverage. Still, they offer different bells and whistles, as well as different rates.

Both Progressive and Geico homeowner’s policies provide medical payments to others in case of injury, liability coverage, and coverage for water or sewer damages. However, Geico and Progressive recommend lower limits of liability and deductibles on glass coverage, where most insurance professionals do not. And both companies offer varying discounts (like paid-in-full discounts, paperless billing discounts, multi-line discounts, and so on).

The biggest benefit of working with an independent insurance agent like Vargas & Vargas is that our licensed, independent insurance agency works with many insurance companies. We know their underwriting criteria and know their ideal customer. Our goal is to spend time with each prospective client to get a feel for your insurance needs. Then we can move forward getting quotes from the best companies for your unique situation.

Need some Massachusetts insurance quotes? Let’s talk!

Liability coverage may be the least understood portion of a typical Massachusetts home insurance policy. Other standard home insurance coverages — like dwellings coverage or personal property coverage — protect you from losses to your own property. In contrast, liability insurance protects you when you’re legally responsible for someone else’s losses.

How the Liability Portion of Your Home Insurance Policy Works

Liability coverage usually extends to you and family members who live in your household. You’re covered if someone sues you or a family member for causing certain injuries or property loss. Liability insurance pays expenses, such as the cost of your legal defense, court costs, and settlement fees (or damage awards).

Examples of What Liability Insurance Can Cover

Your liability protection typically includes accidental injuries to someone visiting your home. For instance, you’re covered if your guest gets hurt from falling on your icy porch steps.

You’re also covered for certain property damage and accidental injuries caused by you or a covered family member that happens away from your home. Here’s an example. Your child is playing baseball in a neighbor’s yard. He pitches the ball, and it accidentally hits the neighbor’s child in the head. The neighbor’s child is seriously injured. Your liability coverage takes care of your attorney’s costs and the settlement fee related to that event.

What Homeowners Liability Insurance Does Not Cover

Liability insurance does not cover intentional acts or injuries. Also, homeowners liability insurance does not cover losses related to the operation of a vehicle or business. You need auto insurance or business insurance for those costs.

Deciding How Much Liability Coverage You Need

For any type of insurance, the coverage limit is the maximum amount of money that the policy will pay out. The coverage limit for the liability portion of home insurance can be as little as $100,000. However, since the median home value in Massachusetts is $426,330, $100,000 is not enough coverage for most Massachusetts homeowners.

You can and should increase your coverage limit to be equal to or more than your home’s value. Losing your home to pay a settlement fee or damage award is a possibility for homeowners who don’t have sufficient coverage. Contact us today so we can help you find a home insurance policy that has the liability coverage that meets your needs.

It’s no secret that the COVID-19 global pandemic has caused immense strain — physically, mentally, and financially. While the uncertainty of the coming months continues to weigh heavily on everyone’s minds, more and more stories are coming to light every day about individuals and corporations trying to do what they can to help. The insurance industry is among them. Several companies have implemented plans in recent days that will attempt to lessen the monetary burden their customers are facing for car insurance and other policies. Wondering if your company is one of them? Check out the list below.

Farmers

Customers with Farmers or 21st Century-branded policies will see a 25% reduction on their premium for the month of April. The discount will be applied as a credit to next month’s billing statement. If you paid your premium in full, it will be issued as a check or direct deposit to the account on file. The reduction is being applied automatically and requires no action on your part.

State Farm

State Farm policyholders will be apportioned part of a $2 billion dividend from the company. While exact percentages for individual customers will vary by state, policyholders will be credited a percentage of their premium from March 20 through May 1. The company estimates that the average will be about 25% of the premium for that time frame, and customers don’t need to take action to receive the credit.

Progressive

Policies active with Progressive at the end of April or May will receive a 20% premium credit. The company will notify its policyholders when the credit will appear, and it will be automatically credited toward the balance of their next bill. If you’ve paid your policy in full, then either a check will be issued, or the amount will be deposited into the payment account on file.

Allstate and Esurance

Through the months of April and May, Allstate and their family company Esurance are offering customers a 15% refund based on their premiums for those months. The money will be directly deposited into whatever account their latest payment was made (or credited to their account) – so no action is required by customers to receive the money. The company is also offering payment relief plans upon request, extended coverage for personal vehicles in certain commercial capacities, and the ability to sign up for free identity theft coverage through 2020.

Nationwide

For policies active as of March 31, 2020, Nationwide will be offering policyholders a one-time premium refund of $50. When you’ll see the money will vary by state regulatory approval. The company is also offering the ability to suspend some cancellations, defer payments for certain policies, and waive some late fees in certain circumstances due to COVID-19 related hardships. While no action is required for the premium refund, you’ll need to reach out to a representative for additional considerations.

USAA

Every member with USAA who has an auto policy in effect as of March 31, 2020, will receive a 20% credit on two months of premiums without needing to contact the company. Extended coverage, policy leniency, and special payment arrangements are also available upon request.

Geico

A 15% renewal discount is being offered by Geico for auto, motorcycle, and RV policies set to renew between April 8 and October 7, 2020, for 6-month policies and between April 8 and April 7, 2021, for 12-month policies. The credit is also being extended to new business policies written between April 8 and October 7, 2020.

No action is required on the customer’s end; the discount will be credited automatically upon renewal. Cancellations due to nonpayment have also been paused through at least April 30, 2020, for all states, while some states may get longer windows. You can see if your state has a longer grace period here.

Liberty Mutual

Liberty Mutual customers with personal auto insurance policies will receive a 15% refund on two months of premiums, based on the premium amount as of April 7, 2020. The refund will be automatically deposited into the account used to make your last payment or by check. When the funds will arrive is subject to individual state regulations, but customers do not have to take any action to receive their money.

Vargas and Vargas Insurance is here to help you. As local independent insurance agents, we represent many local insurance companies that are also offering to lessen the burden when it comes to your automobile insurance premiums. Contact us with your insurance questions or to get a quote. We’re available during business hours at 617-298-0655, or you can reach out through text and online. We take pride in helping you with all of your coverage needs and look forward to taking care of you today.