Make an appointment with your life insurance agent at Vargas & Vargas Insurance to determine the policy benefit your life insurance should provide. We help Dorchester, MA, residents ensure that their life insurance adequately covers the needs of their beneficiaries.

Make a List of Big Things Your Spouse Would Need to Pay Off

Base your life insurance policy benefits on the needs your family would have to cover if you died. Make a list of things your spouse would have to pay for alone if you died. This list might include paying off your mortgage, putting your children through private school and college, and paying off any auto loans your family has open. Your credit card bills and other loans belong on this list, too.

Determine the Loss of Your Annual Income

Your benefits amount should factor in how many years your spouse would potentially live. While your spouse might also maintain a career, a life insurance policy should cover the difference the loss of your income would make. That would ensure your family could continue to live at its current level when you die.

Record Activities You Handle for Your Family

Finally, consider the things you do for your family that they would need to hire another person to do if you died. That might include lawn care, child care, meal preparation, or home repairs.

Parental Care Needs

All of these items vary by person. No two people have the exact same situation, so each person needs to calculate their life insurance needs. If your parents are still living, consider the benefits they would need as they age that they would lose if you passed away. Today, many aging parents move into an addition at their child’s home or relocate to an assisted living center near their child and grandchildren. They may need help paying for this elder care or medical assistance in the house.

Contact Vargas & Vargas Insurance for Life Insurance

At Vargas & Vargas Insurance, we understand the complexities of insurance and work hard to simplify them for our Dorchester, MA clients. Contact us to determine how much life insurance coverage you need based on your family composition and potential beneficiaries.

If you have ever experienced in a total loss of your car, it can be overwhelming. Even experienced drivers can feel panicked when their vehicle is declared a total loss after an accident. Beyond the concerns of injuries and safety, you might have questions about your next steps and the insurance process.

At Vargas & Vargas Insurance, we understand that the aftermath of a car accident is a confusing and uncertain time. Finding out that your car is considered a total loss and won’t be repaired only adds to the stress.

Understanding what “total loss” means and how insurance companies determine it is just one of the many inquiries we receive from clients filing accident claims. We’re here to provide clarity during this challenging period, explaining total loss, how your insurance policy covers it, and the steps you should take afterward.

In this post, we’ll break down when a car is considered a total loss, which coverages come into play, and the necessary actions you should take after experiencing a total loss.

When does a car qualify as a total loss?

If your car sustains significant damage in an accident, your insurance company might label it a total loss. This happens when repairs become impractical or when the vehicle remains unsafe even after fixing it.

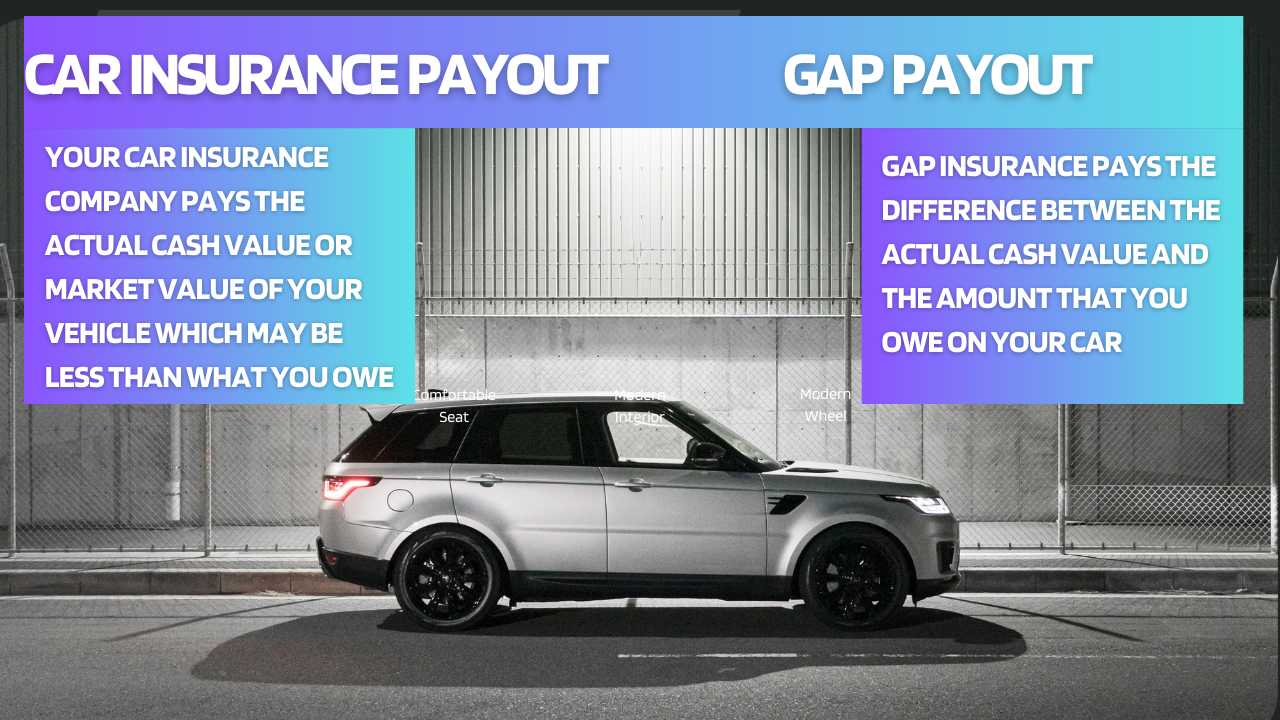

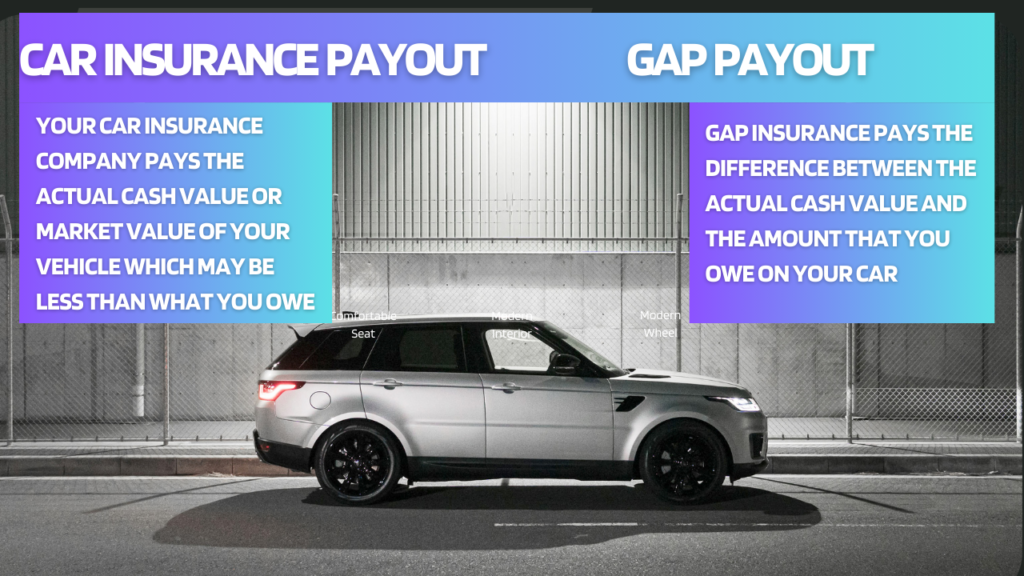

Generally, if repair costs surpass your car’s actual cash value, it’s declared a total loss. Instead of repair expenses, you’ll receive compensation based on the car’s value.

Insurers often take possession of totaled vehicles. Ensure you transfer the title, cancel the license plates, and remove the car from your insurance policy to avoid unnecessary charges.

How do insurance companies decide if a car is a total loss?

Your insurance companies assess if a car is a total loss only after conducting their own inspection of the vehicle’s damages.

Most Massachusetts insurance companies employ the total loss formula (TLF) to decide on total loss status. If the cost of repairs plus the salvage value equals or exceeds the car’s actual cash value, it’s declared a total loss.

Keep in mind that variations exist due to your insurer and unique circumstances, so it’s wise to consult your insurance provider about this process.

How is the actual cash value calculate?

The actual cash value (ACV) reflects your car’s present market worth. Insurers calculate it by subtracting depreciation from the initial purchase price.

It’s important to distinguish ACV from replacement cost. Replacement cost provides the full value of a new vehicle without considering depreciation. However, this coverage is usually limited or comes with higher premiums compared to ACV.

Which insurance coverages deal with totaled vehicles?

If another driver is responsible for an accident that totals your car, their insurance policy will cover your vehicle’s actual cash value.

When you’re at fault for the accident, or if the other driver leaves the scene or lacks insurance, you need to file a claim under the appropriate coverage on your policy to get compensation for your car’s ACV.

The specific coverage you should use depends on the accident scenario:

Collision Coverage:

Handles damages caused by colliding with vehicles or objects.

If you’re at fault for the accident, your ACV reimbursement comes through collision coverage.

Recommended for all drivers but not mandatory in Massachusetts if you own your vehicle outright.

Comprehensive Coverage:

Addresses damages from non-collision incidents like theft, vandalism, weather, and animal collisions.

If a non-collision event results in your car being totaled, the comprehensive coverage is used.

Similar to collision coverage, it’s not required if you own your vehicle and don’t have a loan.

Uninsured/Underinsured Motorist Coverage:

Required in Massachusetts.

If you’re in an accident with an uninsured or hit-and-run driver, this coverage reimburses your car’s ACV.

It’s important to understand which coverage to use based on your accident scenario. If you’re unsure, consult your insurance provider to ensure you’re properly covered.

What happens if I still have a loan on my vehicle?

What if the money you receive for your totaled vehicle doesn’t cover your outstanding loans? This is where GAP insurance comes in. GAP insurance, or “guaranteed asset protection,” fills the gap between the actual cash value you’re reimbursed for your vehicle and the amount you owe on your loan or lease. Remember, GAP insurance is not included by default – you need to add it to your policy through an endorsement if you’re eligible.

How Much Does GAP Coverage cost?

Adding GAP insurance to your Massachusetts auto insurance will typically cost an additional $25 to $75 per year. If you get this coverage through the dealership or finance company, the cost will vary based on factors like the car’s MSRP, loan duration, financed amount, and APR, generally ranging from $500 to $750.

It’s important to note that many dealers and finance companies might attempt to include GAP insurance in your monthly loan or lease payment by default. Therefore, it’s crucial to inquire about this and clarify before finalizing your paperwork.

What steps should I take if my vehicle is declared a total loss?

Here’s what to do if your vehicle is totaled:

File a claim: Contact your insurance agent or provider right away to start the process. Total loss claims are filed like any other claim on your auto policy.

Tow your vehicle: Arrange to have your car towed to an auto body shop since you likely can’t drive it anymore.

Gather documents: Be proactive and collect documents your insurer will need, such as the car’s title and sales receipt. If leased or financed, your lender/lessor will provide the title.

Research car’s value: Look up your car’s current value to get an idea of the reimbursement you might receive.

Check loan status: If you have a loan or lease, inform your lender/lessor about the damages and the upcoming settlement.

Shop for a new car: You may not get the same car, but you can use the reimbursement for a down payment on a new vehicle.

Pro-Tip

Before you do anything, document the condition of your car with photos and notes. This evidence can support your insurance claim and ensure you get the compensation you deserve. Remember, thorough documentation can make a significant difference in a total loss scenario. Stay prepared, stay protected!

Your Local Independent Insurance Broker

Totaling your car can be unsettling, but being prepared is key. Understand what triggers a total loss and how your insurance covers it. This knowledge lets you know exactly what to do if your car is ever totaled.

For over four decades, Vargas & Vargas Insurance has been assisting individuals, families, and businesses. We’re here to address your questions and find the best coverage at the most competitive rates. Reach out to us at 617-298-0655.

If you’ve purchased a new car or leased one, you might have come across the term “gap insurance.” It’s often mentioned during loan or lease paperwork, and you may have been advised to get it from the dealership. However, the explanation might not have been clear.

At Vargas & Vargas Insurance, we’re here to shed light on gap insurance—what it covers, its costs, and the choice between dealership purchase and adding it to your Massachusetts auto insurance policy. (Yes, you heard that right—we might suggest an alternative source!)

While gap insurance is quite affordable when included in your auto insurance, it tends to be pricier if bought at the dealership. But there are distinctions between the two options. Let’s explore the details!

What is GAP insurance?

When your car is in an auto accident, your Massachusetts auto insurance policy covers the vehicle’s “actual cash value.” Keep in mind it doesn’t replace the car itself. This distinction is crucial.

From the moment you drive your new car away from the dealership, its value depreciates. In the unfortunate event of a total loss or theft, your insurance will reimburse the car’s actual cash value at that time. If this amount falls short of your loan or lease, you could still owe money. This is where GAP (Guaranteed Asset Protection) insurance comes into play – it bridges this gap, covering the difference.

Who Can Purchase GAP Insurance?

GAP insurance can be added to an auto insurance policy within 30 days of purchase of vehicle. But it’s important to note that if you have an accident before that 30 days is up, and you haven’t added the coverage yet, you will not be able to add it after the accident.

You also must have bought the vehicle using a loan or lease, and the vehicle must be 5 years or newer to be eligible.

Is GAP Insurance Mandatory?

While not mandated by the state of Massachusetts, GAP insurance is not a requirement for all drivers. However, if you’re leasing a vehicle, the leasing company might insist on this coverage. Checking your lease agreement will provide clarity on whether it’s necessary. To understand the impact of leasing on your auto insurance, feel free to reach out for more information.

How long do I need to pay for GAP insurance?

The duration of your GAP insurance coverage depends on your individual circumstances. Generally, it’s advisable to have GAP insurance throughout the entire duration of your auto loan or lease. This way, you’re protected in case of a total loss or theft. However, you can consider cancelling the coverage once the gap between your loan/lease balance and the vehicle’s value decreases significantly. To make an informed decision, discuss your situation with your insurance provider.

What Does GAP Insurance Cost?

By including GAP insurance in your Massachusetts auto insurance policy, you’ll likely see an increase of around $25 to $50 in your annual premium.

However, if you opt for dealership or finance company coverage, the cost will fluctuate based on factors such as MSRP, loan duration, financed amount, and APR. Generally, this option might range between $500 and $750.

Be aware that some dealers and finance firms might automatically bundle GAP insurance into your monthly payment. To avoid surprises, make sure to inquire about this before finalizing your paperwork.

Your Local Independent Insurance Broker

Vargas & Vargas Insurance has assisted individuals, families, and businesses for over four decades. We’re here to address your questions and find the best coverage at the most competitive rates. Reach out to us at 617-298-0655.

How does saving thousands of dollars in car repairs sound?

We’re here to share some maintenance tips that may do just that! Check them out below:

Schedule Inspections and Maintenance

To save money on car maintenance, regularly book check-ups and services. Think of it as preventative maintenance to avoid costly repairs later. For instance, replacing brake pads is cheaper than replacing damaged brake discs. How often you should have your car checked depends on how much you drive – more miles mean more frequent check-ups.

Change The Oil – To keep your gasoline-powered vehicle running smoothly, it’s important to regularly change the oil. This typically costs around $60 and should be done every 5,000 miles. Even if you don’t drive much, you should still change the oil at least once a year, according to Consumer Reports.

Keep The Battery Clean – If you don’t keep it clean, it could develop a crack or not function properly. Test your battery twice a year and inspect it for corrosion.

Replace The Brake Pads – Check the brake fluid every time you change the oil. If it’s dark in color, reach out to a mechanic to get your brake fluid changed and see if a new system is needed.

Replace Your Air Filter – Change your air filter every 12 months or 12,000 miles, as using an old air filter can lead to significant – and costly – problems for your air conditioning system.

Lights On For Safety – Keep a close eye on your car’s lights. Make sure your headlights, brake lights, and indicators are functioning properly. Don’t forget to test the brake lights by pressing the pedal or asking for help. Modern cars have a warning light on the dashboard to signal when lights are out. Remember, faulty lights can be dangerous and might lead to fines from the police. Stay safe on the road!

Here’s A Pro-Tip – According to auto mechanic expert Scotty Kilmer, tire rotation for modern cars is an unnecessary expense. He explains that today’s tires are significantly superior to those in the past.

Your Local Independent Insurance Broker.

If you want to ensure that you have the best insurance coverage at the most affordable price, our team is ready to assist you. Simply dial 617-298-0655 to get in touch with us. We will be happy to review your insurance policy and make recommendations to ensure that you are properly insured.

Do you need a new insurance agent or broker? Maybe you’re unsure and looking for advice or wanting to switch agents. It’s important to choose the right one, so it’s wise to do your research and evaluate potential agents. Not all agents and brokers are the same. How can you distinguish a good agent from a bad one?

What are the benefit of changing my agent after having worked with the same one for a long time?

Your insurance agent may not be good even if you’re used to them. You may have outgrown them as your needs change over time. You might be missing out on savings if you’ve been with the same agent for a long time. Switching agents can help you find better deals and stay up to date with industry practices. It’s important to work with an insurance broker who will review your insurance annually, compare quotes, and recommend alternatives when it’s time to switch insurance companies for more favorable rates. At Vargas & Vargas Insurance, we do this for ever client every single year.

What Is An Independent Insurance Brokers

An Independent insurance broker does not work for a single company but instead serve clients in finding coverage from a network of insurers. Unlike agents who are tied to one company, like Allstate, Liberty Mutual, AMICA, GEICO and many others, independent brokers have the flexibility to work with multiple insurance providers to find the best coverage options and rates for you. They have no vested interests in promoting a particular company, so you can trust that their recommendations are based solely on your needs. Whether you need help navigating a life change or simply want advice on switching to a new car insurance provider, independent brokers are there to provide unbiased advice and help you make informed decisions.

What Is A Captive Insurance Agent

Agents who work exclusively for one insurance company are called captive insurance agents. They are obligated to sell their company’s insurance policies, regardless of whether it is the best fit for the customer. If you choose to work with a captive insurance agent, you may not be getting the best possible insurance coverage or rate. This is because they will only offer you rates that are available through their company, and not necessarily the most affordable options. They are not motivated to help you switch to another insurance company, as their commission is tied to providing good customer service for their company. While they may strive to provide excellent customer service, their primary concern is the success of their company, not the satisfaction of their clients.

Buying Insurance Online

If you lack knowledge about insurance, buying your insurance online can be perplexing. And sometimes, there may be some fine print or confusing legal jargon that you might miss. However, if you choose to use an insurance agent, we can assist you in deciphering all of those details. Even though some online companies call center agents, they may not be able to provide personalized service, and you might end up speaking with multiple people. This can be a problem because if you’ve already explained your concerns to one agent, the next agent you speak to may not have that information, and you’ll perhaps have to start from scratch.

Finding The Right Insurance Broker Or Agent For Your Needs

Do your homework. Find a broker or agent who genuinely cares about your interests. With numerous options available, it’s tough to choose, especially when every one of them claims to be the best.

Check out reviews and recommendations. Start by talking to people you know, like, so you can trust their feedback. Who did they have a positive experience with? Who do they advise you to steer clear of? These suggestions matter.

If personal recommendations don’t help, go online. Look for insurance agents’ ratings and reviews on platforms like Google, which can guide potential customers. Additionally, when reviewing online reviews, check if the business responds to its reviews. A business that values its clients and reputation will engage with the feedback they receive.

To learn about the insurance options offered by Vargas & Vargas Insurance, you have a few options. You can reach out to an agent by calling 617-298-0655, visiting their website at vargasinsurance.com/contact-us, or even sending a text to 617-409-0329. The team is ready to assist you with any inquiries or issues you may have.